We're in trouble, deep trouble, and nobody is talking about it. "Jobs and Boats" is a side-show, the Good Times are well and truly over: we need to address hard questions or we'll be hammered.

If you think 8 years on from the GFC, still with record-low interest rates, heading down to 1%, signals anything but a fragile economy on its knees, facing "falling off a cliff" from the slightest nudge, you haven't been paying attention... If this were a plane crash, we're in the last few hundred feet while the 'pilots' are working hard to avoid it, while over the PA they're saying "we have a slight problem".

The key to our future is "The New Economy". The chief enabler for it is simple: Fast, Real Broadband, everywhere. Any technology that buffers, 'breaks-up' pictures/voice or has long delays is not 'Real Broadband'. The NBN matters to our future now, more than at any other time.

The major Political Parties yammer on about "Debt & Deficit", Tax Cuts and funding Health & Eduction as if its 2006, when so much money was pouring into Treasury, Howard/Costello had problems spending it all.

Howard received at least $575 billion in extra-ordinary one-off revenue and his headline result was to turn a debt of $96 billion into a $20 billion surplus, while halving infrastructure spending, killing moves for an NBN and creating a monumental structural deficit. The other $460 billion was just given away in tax cuts, not saved, not invested, not used to create a Fund for future generations - they just squandered it all, in what the OECD called the most 'profligate' period in our history. Howard bought election wins with our future.

Howard/Costello did not setup Australia with the giant one-off lottery win we had, they did the opposite, they squandered a temporary boom, creating permanent tax cuts and sabotaging our economic & social future.

Howard/Costello left the electorate with a fatal triple set of expectations:

- Every election, there will be Tax Cuts.

- The only measure of 'Good' Economic managers is they produce surpluses. "Debt and Deficit" are somehow evil, not a reflection of external factors and tax give-aways.

- We're somehow 'Golden', we are recession proof and our House prices can rise forever.

Their major Policy platform is "A Strong New Economy". I encourage you to read it, it takes most time to scroll down to find 'the Plan' than to read it.

The Amazing Turnbull Plan is a bunch of bullet points filled with a string of vapid, vacuous content-free phrases. There is nothing new there, supported with no modelling, no figures and targets/goals. There are no links to any supporting documents.

This is a Party in Government, not Opposition. They've had the full resources of Treasury and Finance at their disposal for years to create credible forecasts for their policies. The best evidence the Liberal-National Coalition can provide is slogans and endless repetition of dogma. That alone is a strong red flag.

The real Red Flag is their parlous performance as both legislators and economic managers.

What happened when "The Adults were back in charge"? A disaster in the Senate! They still have legislation from 2014 languishing there and unlikely to ever to be passed.

The Gillard minority Government did not have this problem. They had an even worse situation, needing to effectively negotiate with the cross-bench in both houses - that's what Good Government looks like. Politics is famously "The Art of the Possible", not "Crash or Crash Through".

Having a dummy spit and blaming everyone else when you can't get your own way is not "Adult" or "Good Government". Abbott fell out of favour with the public, causing his Party to dump him, for a simple reason: he could not do the job required.

Prime Ministers need to negotiate, not dictate, compromise not stone-wall and they cannot blame others. The buck stops with the PM. If they cannot achieve their Policy Agenda, they are the wrong person for the job.

From Turnbull's underwhelming performance and major policy backflips since the September "disagreement" (the Libs don't call it a Leadership coup now), we can surmise that the problem wasn't solely Abbott or Credlin, but the Party Room.

There is no Budget problem in Australia, we don't have a Revenue or Expenditure Problem, we have too many Tax Giveaways. We'd have a $70 billion surplus today, if we stopped giving away money hand-over-fist to a privileged few. Politicians haven't had the courage to address this head-on.

We are "living beyond our means", ever since Howard squandered our birthright, but its not an imbalance of Revenue & Expenditure. It's the money we don't collect that's killing us. We need to reign back the Freebies, the pork-barelling and Gifts/Giveaways to the already wealthy.

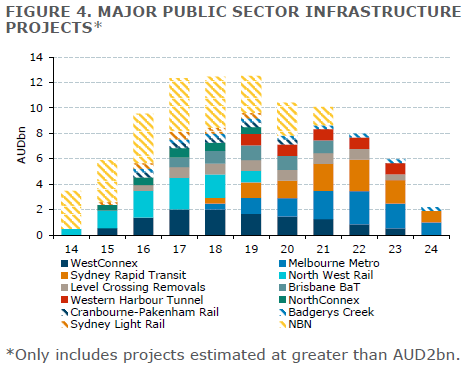

Infrastructure Spending.

Some articles:

Quigley: Turnbull butchered the NBN, 23 June 2106.

Reserve Bank Australia, Chart Pack, June 2016

or PDF

|

| Public Construction Work Done. Percent Nominal GDP |

Trends in infrastructure

Greg Coombs and Chris Roberts

Treasury, 2005

http://archive.treasury.gov.au/documents/1221/PDF/01_public_infra.pdf

http://archive.treasury.gov.au/documents/1221/HTML/docshell.asp?URL=01_public_infra.asp

ABS Data: http://www.abs.gov.au/ausstats/abs@.nsf/mf/8762.0

The adequacy of Australia’s infrastructure has been a long-standing topic of debate.The very long run

This article provides some insight into the question of infrastructure adequacy by examining trends in investment across OECD countries, and discusses some of the fundamental factors influencing Australia’s investment relative to other OECD countries.

The article also looks at the question of the changing composition of public and private infrastructure spending in Australia over recent decades.

In broad terms, through the period from Federation to the present, total fixed capital investment as a proportion of GDP has fluctuated widely from around 3 per cent of GDP to around 19 per cent of GDP.

|

| Chart 1: Ratios of total and public investment to GDP: 1901-2005 |

Recent times

Chart 2 takes a closer look at a recent period — from June 1987 to June 2006 — for a sub-set of fixed capital expenditure — investment in economic infrastructure. Economic infrastructure covers utilities and non-dwelling construction.

Investment in economic infrastructure stood at 4.5 per cent of GDP in June 2006, compared with 3.2 per cent in June 1987.

|

| Chart 2: Investment in economic infrastructure by sector As a percentage of GDP |

Underlying these trends is that infrastructure investment as a proportion of GDP reflects efficiency gains in the provision of new public investment, as productivity levels in construction increased in the late 1990s compared with historical trends (Dolman et al, 2006).

|

| Chart 4a: Total net capital stock to GDP ratio in selected OECD countries at 2000 purchasing power parity, in US dollars |

|

| Chart 4b: Government net capital stock to GDP ratio in selected OECD countries at 2000 purchasing power parity, in US dollars |

Construction activity to hit real GDP growth

Wednesday, May 25, 2016

Callam Pickering

http://www.cpeconomics.com/#!Construction-activity-to-hit-real-GDP-growth/c1tye/574505aa0cf2123d26b4283d

The volume of construction work done fell by 2.6 per cent in the March quarter, missing market expectations, to be 6.7 per cent lower over the year. Construction has fallen 14.5 per cent from its peak in the December quarter 2012.

Weakness was driven by a combination of non-residential building and engineering construction. Non-residential construction fell by 5.5 per cent in the March quarter, while engineering (a proxy for mining) construction fell by 4.2 per cent. Engineering construction has fallen one-third from its peak.

g

gPublic sector construction increased for the third consecutive quarters, up by 3.1 per cent in the March quarter on a trend basis, but is still 34.5 per cent below its peak almost six years ago. New infrastructure projects should support public construction activity in the near to medium-term. Private sector construction is down 10 per cent over the year, with further weakness to come as engineering construction deteriorates and residential construction activity peaks.

My models suggest that private residential investment in the national accounts should increase by 1.5 per cent in the March quarter; while non-residential construction could decline by 6.1 per cent. Combined these sectors are expected to subtract 0.2 percentage points from real GDP growth in the March quarter. The true subtraction from construction though could be as high as 1.0 percentage point once we include engineering construction.

The outlook for construction activity remains fairly bleak. The public sector is obviously a bright spot but engineering construction still has a long way to fall and residential construction is rapidly approaching its peak. Don't be surprised if we see a bit of a squeeze on construction jobs.

Wage growth falls further to fresh record low, construction work weakens: ABS

Stephen Letts

24 Feb 2016

http://www.abc.net.au/news/2016-02-24/wage-growth-falls-further-to-fresh-record-low/7196002

Wage growth has fallen to a record low of just 2.2 per cent a year.

On a seasonally adjusted basis, the Australian Bureau of Statistics wage price index rose an insipid 0.5 per cent in the December quarter.Building and construction faces a tough time as pace slackens

This is another step down from the September quarter's wage price growth of 0.6 per cent.

The ABS noted it was the lowest annual wage growth since the series started in 1998.

Wage growth slowed across most industries when compared to the same quarter last year.

Not surprisingly, the smallest quarterly rise for all industries was in mining, at just 0.1 per cent.

Financial and insurance services recorded the largest quarterly rise of all industries at 1.1 per cent.

Public sector wage growth of 0.6 per cent for the quarter slightly outpaced the private sector at 0.5 per cent.

Private sector wages are up just 2 per cent over the year.

ANZ economist Justin Fabo said wage growth is likely to remain subdued for some time due to a number of factors, including spare labour market capacity, low inflation expectations and the downward pressure on Australian incomes from falling terms of trade.

"Subdued wages growth has been supporting jobs growth overall but household income growth has remained weak," Mr Fabo said.

"We expect modest improvement in wages and household income growth, and hence consumption growth, over the year ahead.

"But we struggle to see annual growth in household spending returning to 3.5 per cent rates as per the RBA view."

That is likely to keep downward pressure on inflation, leaving it near the bottom of the Reserve Bank's 2 to 3 per cent target this year.

Construction work dragged down by engineering

Construction work has fallen 3.6 per cent in the December quarter, driven down by a collapse in large-scale engineering work.

The total value of construction work in the quarter came in at $48.4 billion on ABS estimates.

In seasonally adjusted terms, total construction across all across all sectors was down 4.3 per cent over the year.

The value of engineering work fell 9.5 per cent in the quarter and almost 15 per cent over the year, more than outpacing gains in building and residential work.

Residential and building construction were up 8 per cent and 11.5 per cent respectively year-on-year.

CBA's Gareth Aird said the decline in construction work was much greater than the market expected.

"The breakdown by public and private sectors shows that the much hyped lift in public sector infrastructure has yet to occur," Mr Aird said.

"Despite there being plenty of talk around big investment in public infrastructure the data shows that it simply isn't the case, at least at the national level.

"Public construction work done was flat over the year and has been making a negative contribution to GDP growth since 2010."

AMP Capital's Shane Oliver said, while this means that dwelling investment will be a positive contributor to December quarter GDP growth, business investment is likely to remain negative as the unwind of the mining investment boom continues to weigh.

"Today's wages and construction data are unlikely to have been weak enough to bring on a rate cut from the RBA next week," Dr Oliver said.

"But they are both consistent with the RBA retaining an easing bias and likely acting on it sometime in the next few months."

FRANK GELBER

23 JUNE, 2016

http://www.theaustralian.com.au/business/property/building-and-construction-faces-a-tough-time-as-pace-slackens/news-story/4fc5f9de7e26d42f3fe6a5dbc0a74168

After the heady days of the mining investment boom, this is a difficult time for those involved in the building and construction (B&C) industry. It faces significant cyclical shifts in the context of an overall decline. Nevertheless, some sectors will do well as others decline. Just as some regions will do well as others decline.

Let me give you some orders of magnitude.

During the 10-year mining boom, total B&C doubled, driven virtually single-handedly by mining investment. That’s a huge boost to the domestic economy, both directly and with a strong multiplier effect through the rest of the economy.

It was punctuated by the GFC:

● In the private sector by the pre-GFC financial engineering boom and post-GFC bust;

● In the public sector by the post-GFC stimulus package and subsequent cuts in expenditure; and

● By the effects of budget constraints operating to reduce public construction by 25 per cent over the last five years.

Now, we’re paying the price for the mining investment boom with mining construction half way through a forecast 72 per cent decline. Certainly, infrastructure spending is set to rise by around 20 per cent over the next four years. But, overall, engineering construction will fall by another 20 per cent over the next few years.

Meanwhile, the residential building boom has run its course as pressure on investors is impacting on the bankability of high-rise projects and will be contributing negatively to growth from next year as work done falls by around 20 per cent over the next three years.

So far, no good.

What about non-dwelling building? Work done has been drifting downwards for most of this decade.

We’ve now just about unwound the government’s post-GFC package, though some large hospital projects remain to be completed. Social and institutional building is near the trough of the cycle and will start to pick up, though not dramatically. Our commencements forecasts point to increased expenditure in the health, education and aged care sectors.

Commercial and industrial building, too, is near the trough. Retail and industrial have been relatively steady, with strong investor interest, but with development limited by demand in a weak economy. Building will pick up pace only when non-mining investment leads to a strengthening of the economy.

Hotels building is more cyclical, with insufficient building post-GFC leading to a shortage of hotel space to service business travellers, in turn sparking a dramatic building boom in the cities — just in time for the resources downturn. That will cause significant oversupply as demand drops in Perth, Darwin and Brisbane, though mitigated to the extent that increasing tourism will absorb some of that stock.

Sydney and Melbourne have overbuilt, too, but demand will be sustained. And we haven’t built much in the tourism areas yet — that’s where the demand will be as both inbound and domestic tourism, buoyed by the lower dollar, pick up momentum into what will be a boom in five years time. Sydney, Melbourne, Hobart and Brisbane will pick up shares of that demand. Accordingly we expect the strength of hotels building to switch to the tourism regions.

Office markets are the most cyclical. Building commencements have fallen sharply.

The Brisbane, Perth and now Darwin markets kept building at boom levels while demand fell with mining investment. A quarter of Brisbane’s office space, and half of Perth’s, is occupied by people servicing mining. Those markets are significantly oversupplied and building is collapsing with little prospect of a near term recovery. There’s plenty of space in Canberra, with government departments having underwritten new buildings as their leases expired — leaving swathes of empty secondary space. Building there will depend on government willingness to commit to new leases in new buildings. But I wouldn’t like to own one of the empty ones.

Melbourne is steadier, with solid and increasing demand absorbing continued building. It will do well.

In Sydney, developers were frightened off by the Barangaroo development, leaving a post-Barangaroo gap in building. The emerging shortage of space will underwrite strong rental increases and a new round of development. But we won’t get significant space onto the market for another three years yet. With solid demand and with net absorption limited by the availability of space, rents will continue to rise. There’s a boom coming for both property and building.

Non-dwelling building commencements have already begun to rise from the recent trough and will continue to rise even in a soft economy, picking up pace as the economy strengthens.

Even so, there will be marked differences in performance by city and state. But that won’t be enough to offset the weakness of residential building and non-building construction.

Overall, total B&C will continue to decline for another three years. We are not even half way into a 27 per cent decline. We’ve had sharper episodes in the past — in 1982, in the early 1990s and in 2001 but they haven’t been as sustained as this one. Just as in the overall economy, there are emerging growth sectors. But first we have to absorb the effects of falling mining investment. This will be a difficult time for the construction industry. And they’ll need to be nimble to negotiate the structural shifts and cyclical swings.

Frank Gelber is chief economist BIS Shrapnel.

No comments:

Post a Comment